* This article was originally published on August 12, 2020. It has been updated for 2023.

What’s the best way to give money to kids? With school having started last week here in Fort Collins and the back-to-school season ramping up for many ahead of the Labor Day weekend, it’s a hot topic!

Whether it’s giving to kids, grandkids, nieces, nephews, or other special little ones in your life, we get this question quite a bit. And with the SECURE 2.0 Act allowing for rollovers from 529 Plans to Roth IRAs starting next year, we decided to turn our three-part series on “Giving Money to Kids” into an all-inclusive piece.

From college savings strategies to gifts that are not necessarily for education, you’ll find it all right here.

Primarily, the questions we’ve gotten have focused on where the best “place” to put money for little ones is. What’s interesting about this question is that there are so many potential answers that the options can actually get a little overwhelming. From simple “mental accounting” — i.e., $X in this account is for Jr.’s college — to elaborate trusts and everything in between, the solutions are practically endless.

However, I do think there are a few strategies that won’t necessarily numb the mind and are certainly worth considering. The first thing to ask yourself when this topic comes up is, “Do I want this money to be used specifically and only for college?”

If the answer to both of those is yes, then you should really focus on the tax benefits available when saving for college.

Education Giving

The current granddaddy of investing for college is the Section 529 College Savings Plan. Because of its popularity, I want to start here. And while that doesn’t mean that I think this is necessarily the best place for college savings, the future Roth IRA rollover option certainly makes it a bit sweeter. Let’s explore what a 529 Plan is and how it works.

The 529

How do 529 Plans Work?

You’ve probably heard of a 529 Plan, but you might be wondering, “How do 529 plans work?” 529 plans are state-sponsored college savings plans that allow for money to be invested on a tax-deferred basis. That means there are no taxes on dividends, interest, or capital gains when earned in the account.

When money is distributed from the account, if the money is used for qualified education expenses, it is withdrawn tax-free. Recent changes to tax law expanded the types of expenses that 529 money can be used for, which now include private K-12 education, for example.

Limits exist on the types of investments that can be used in a 529 plan — typically mutual funds and bank products — and how often those investments can be changed.

There is no federal tax benefit for contributing to a 529 plan. However, in the state of Colorado — and several other states — you can generally deduct your contribution for state income tax purposes if you contribute to a plan sponsored by the state. For the purposes of the Free Application for Federal Student Aid (FAFSA), 529 plan assets are generally treated as the parent’s assets. This is important because, under the federal aid formula, the parent’s assets are viewed as “available” for college expenses at nearly 1/4 the rate of the student’s assets — 5.64% vs. 20%, respectively — and making them less “available” means potentially more available aid.

There is good and bad with a 529 plan. Probably the top gripe I hear is the availability of investment options. When faced with this decision-making process in practice, if, for whatever reason, a 529 college savings plan doesn’t seem like the right vehicle, three other avenues are typically left to explore. Each of the three maintains some form of tax benefit, which I think is the most important consideration once you’ve decided that the money will be used for education.

SECURE 2.0 Act: 529 Plan-to-Roth-IRA Rollover

As for the aforementioned 529 Plan-to-Roth-IRA rollover option, there are a few key points to be aware of to understand how it works. The first is that it’s limited to $35,000 in total rollovers. That’s a nice chunk of change to kickstart a kiddo’s retirement savings!

However, those rollovers are limited to the child’s income or the IRA contribution maximum for the year, whichever is less. So they have to be of working age and actually earning income to roll funds from their 529 Plan to their Roth IRA. That aligns pretty nicely with the minimum employment age, but it’s important to note that the 529 Plan account also has to be open for 15 years before the first rollover can happen. Add to that the limited amounts allowed annually, and you’re looking at another five-odd years to complete rollovers up to the limit value, based on the 2023 Roth IRA contribution maximum. Altogether, that’s 20-plus years to reach the full $35,000!

Unfortunately, that doesn’t allow for much time to get those funds into a Roth IRA before age 18, depending on timing. So the impact as far as “giving money to kids” is rather limited and likely better as a backup plan for those who don’t use all of their 529 Plan funds on education as children or college students. For adults and kids who meet the criteria, rollovers from 529 Plans to Roth IRAs are allowable beginning January 1, 2024.

Coverdell

Then there’s the Coverdell Education Savings Account. A Coverdell is somewhat of a quirky account type; look at it as a hybrid between a Roth IRA and a 529 plan with its own unique set of rules.

Up to $2,000 can be contributed to a Coverdell for the benefit of an under-18-year-old annually. The money can be invested into effectively anything a regular brokerage account could be invested in, which is much more accommodating than a 529 plan. Although the contributions are not deductible, the money in the account does grow tax-deferred and, if it’s withdrawn to pay for primary, secondary, or post-secondary education expenses, it is tax-free.

Like a 529 plan, Coverdell money can be used for private elementary and high school tuition as well as even less direct education-related expenses, like a computer for school. However, unlike a 529 plan, income thresholds may limit contributions to a Coverdell. If your Modified Adjusted Gross Income (MAGI) is greater than $110,000 or $220,000 (single or joint, respectively), you can not contribute to a Coverdell at all. Also, when the designated beneficiary reaches age 30, the beneficiary must be changed to someone under the age of 30 to avoid taxes and penalties.

Other Giving Options

IRAs

But let’s say that you’re exploring for a more creative solution and, even though you believe this money will be used for education expenses, you’re not entirely sure. Even more, let’s say that you’re not entirely sure you’d like to “give” this money to a child for any specific purpose, at least not today.

Interestingly enough, your Traditional and/or Roth IRA can serve as a pretty tidy education fund to accommodate these thoughts.

Traditional

With a Traditional IRA, you can look at distributions you take to pay for “qualified higher education expenses” for yourself, your children, or your grandchildren as a “normal” distribution, regardless of your age. This is because the circumstance is an exception to the 10% premature distribution penalty tax.

If your contributions to the IRA were deductible or rolled over from a deductible employer-sponsored plan, like a 401(k), then the distribution is still taxable as income. If your contributions were non-deductible — and this is specifically a great use of a non-deductible IRA — then only the portion of the distribution attributed to growth would be taxed while the remainder would be treated as a tax-free return of principal.

Remember: In both cases, you also potentially have had years of tax-deferred growth.

Roth

Roth IRAs continue down a similar path as non-deductible Traditional IRAs, except for one key difference. The way the rules for distributions from a Roth IRA are written, it’s always your principal that comes out first. What this means is that you could take distributions to pay for higher education expenses — or literally anything — and those distributions would be tax-free.

Once you do go above the amount you put into your Roth IRA, and assuming any Roth IRA for you has been open for five calendar years, then your distributions are taxable. But again, there is no 10% premature distribution penalty tax because of the exception to the penalty discussed above.

Downsides to Using an IRA for Education Funding

Keep in mind that, although this can work out well depending on your circumstances, there are a few key drawbacks to using your IRA as a college fund. First, even though an IRA balance is sheltered from the federal aid formula as an asset, the distributions are treated as income and work their way back into the formula there, affecting aid for the following school year.

Second, and this is true of a 529 plan and a Coverdell, the distribution must be taken in the same year that the expenses occur. They can not be used to repay student loans or prior expenses.

Finally, remember that the purpose of an IRA is a retirement savings vehicle. Once the money is out to pay for college expenses, it’s no longer earning returns, and the only way to get money back in is through normal, capped contributions.

Finally, we’ll look at giving money when education isn’t the primary concern. Perhaps you want to provide a financial head start to your kids once they become adults — maybe so each can start a business or buy a home. Maybe you’d even like the money to be used for college or other education expenses … but you aren’t sure if that’s the path your kids will take.

To be candid, it’s really difficult to know exactly what will happen five, 10, or 15 years from now. The only thing you can do is consider all your options and make an appropriate planning decision with that information.

Non-Education-Specific Giving

Here is where non-education-specific gifting comes into play. In reality, only a couple of practical options exist when it comes to just flat out giving money to a minor:

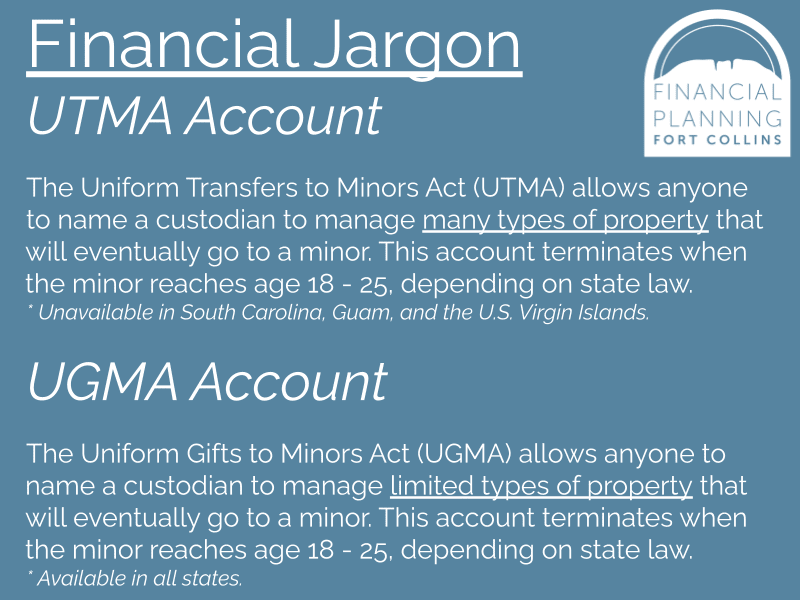

1. An operation of law, called either a Uniform Transfers to Minors Act (UTMA) account or a Uniform Gifts to Minors Act (UGMA) account.

2. Placing the gift in trust for the minor, with the most common being the Section 2503(c) trust, aka a “Minors trust.”

The key distinction between the two is that the former — an UGMA or UTMA account — is very simple and virtually cost-free to establish while the later — a Minors trust — will likely require the work of an attorney.

Minors trust

Starting with the latter, a Section 2503(c) trust gets its name from the section of the Internal Revenue Code that makes its establishment an option. The purpose of a Section 2503(c) trust is to give money to a minor that he or she may not use immediately but have the gift still qualify for the annual gift tax exclusion amount, which is $15,000 for 2021. Normally, only amounts that are given in what is called “the present interest” would qualify for the annual gift tax exclusion.

Typically, the trust will offer a period of time after the minor turns 21 for the beneficiary to remove principal from the trust. After that period of time, if property remains in the trust, stipulations in the trust document dictate how property can be removed in the future. However, after this period of time, gifts to the trust no longer qualify for the annual gift tax exclusion amount. Beyond the cost of an attorney to draft the document, probably the largest drawback to a Section 2503(c) trust is that, by default, it is taxed as a separate entity at higher trust tax rates.

UGMA and UTMA

As for UTMA and UGMA accounts, all states except for South Carolina recognize an UTMA account as a form of property ownership. This is important because an UTMA account can hold virtually any asset type, including real estate. An UGMA account, on the other hand, is limited to bank deposits, securities — think stocks, bonds, and mutual funds — and insurance policies.

Gifts to UTMA and UGMA accounts also qualify for the annual gift tax exclusion amount. With both account types, state law dictates the age at which a minor becomes an adult; in most cases, either 18 or 21 (in Colorado, it’s 21). Usually, the law of the state where the UTMA or UGMA was established or where the minor lives applies.

Taxation of UTMA and UGMA accounts falls under the “kiddie tax” rules. In 2020, the first $1,100 of unearned income is tax-free to a child, the next $1,100 is taxed at the child’s rate, and anything above $2,200 is taxed at the parents‘ highest tax rate. While this provides some tax relief, managing for tax issues is important if the account has the assets to possibly generate more than $2,200 in income or capital gains.

For all of the non-education-specific funding arrangements: a caveat.

Unlike the education savings vehicles and strategies discussed earlier in which a beneficiary or intended recipient can be changed, gifts to minors under the circumstances we’ve just covered here are irrevocable. With the Section 2503(c) trust, the asset belongs to the trust and, eventually, the minor. With an UTMA or UGMA account, the asset immediately belongs to the minor with an adult custodian until the child reaches the age of majority. However, in these cases, money can be used prior to the age of majority as long as it is for the benefit of the minor. This can be for education — or it can be for braces or a trip to summer camp.

Therein lies the tradeoff: rigidity and tax breaks or flexibility and few tax benefits.

If you’d like to talk through any of the options above — or another, like making a child the beneficiary of one of your accounts — feel free to schedule a meeting. We can even guide you through setting up some of the aforementioned accounts, including preparing paperwork for you to establish a traditional IRA, Roth IRA, or UTMA. If you’re considering a section 529 plan or Coverdell ESA, let us know so we can add it to the education funding tab of your financial planning app. And if you’re planning to meet with an attorney to create a Minor’s trust, we’re happy to sit in on the meeting with you.

And don’t forget that gifting the money is only one side of the equation. What the child will do with that gift is another. If you’re looking to impart a bit of financial wisdom to your gift’s young recipient, our blogs on going from a piggy bank to the real bank and turning money education into a game may help.

Happy giving!